%20file.png)

How to Value a Company in the UAE

- Credence & Co

- Nov 18, 2025

- 17 min read

Updated: Dec 5, 2025

Valuing a company is where financial science meets business intuition. It’s a process of forecasting a company's future earnings while also seeing how it stacks up against its peers. The three main ways to get this done are the Discounted Cash Flow (DCF) method, Comparable Company Analysis (CCA), and the Asset-Based Approach. Each gives you a different, yet essential, piece of the puzzle.

Why Company Valuation Is More Than Just Numbers

Before we get tangled up in financial models, let's get one thing straight: a good business valuation is a story backed by data, not just a number spat out by a spreadsheet. The numbers are the foundation, of course, but they can't tell you everything. At its heart, valuation is about pinning down a company's economic worth, a crucial step for almost any major business decision.

Figuring out what a company is worth is fundamental for all sorts of strategic moves. Whether you're eyeing a merger, hunting for investment capital, planning your exit, or just trying to decide where to put your resources, a solid valuation gives you the confidence to act. It turns vague business goals into something tangible and defensible.

The Art Behind the Science

The real "art" in Company valuation comes from interpreting the narrative hidden within the financials. It's why two analysts can look at the exact same data and come up with different valuations—they're weighing the qualitative factors differently. These intangibles are often where the most significant value lies, but they're also the trickiest to pin down on a spreadsheet.

Think about these powerful, non-numerical drivers of value:

Brand Reputation: A killer brand lets you charge more and keeps customers coming back, which feeds directly into future revenue.

Management Team Strength: A sharp, experienced leadership team can execute a plan flawlessly, which lowers risk and gets investors excited.

Market Position: If you dominate your market or have a unique edge, you're naturally worth more than a company just trying to stay afloat in a crowded space.

Intellectual Property: Things like patents and proprietary tech can build a wall around your business, protecting your profits from competitors for years to come.

A great Business valuation tells a compelling story about a company's future, grounded in the reality of its present. It's about building a case for what the business could become, not just what it is today.

Introducing the Three Lenses of Valuation

Pros rarely ever stick to just one method. To get a truly robust valuation, you need to look at the company through three different lenses, each giving you a unique perspective on its worth. Knowing which one to use, and when, is the key to landing on a number that’s both fair and accurate.

First up is the Discounted Cash Flow (DCF) method. This one looks inward, zeroing in on the company's ability to generate cash down the road. It’s all about finding the company's intrinsic value.

Next, we have the Comparable Company Analysis (CCA). This approach looks outward, benchmarking the business against similar companies that are publicly traded. It gives you a market-based, relative value.

Finally, there’s the Asset-Based Approach, which tallies up the tangible and intangible assets sitting on the balance sheet. This is especially handy for asset-heavy businesses or in scenarios like a liquidation. For business owners looking to boost their bottom line, unlocking business value through a deeper understanding of these assets is a critical next step.

By weaving together the insights from all three approaches, you start to build a much more complete and defensible picture of what a company is truly worth.

Building Your Discounted Cash Flow (DCF) Model

When it comes to valuing a business, the Discounted Cash Flow (DCF) model is a true cornerstone of the discipline. The core idea is simple but incredibly powerful: a company's real value is the sum of all the cash it will generate in the future, with a slight adjustment because money tomorrow isn't worth as much as money today.

What I appreciate about the DCF method is that it forces you to get your hands dirty. You have to really dig into a company's operations, its growth potential, and all the risks it faces. It's a method that cuts through market noise and gets right to the heart of what drives a business's fundamental worth.

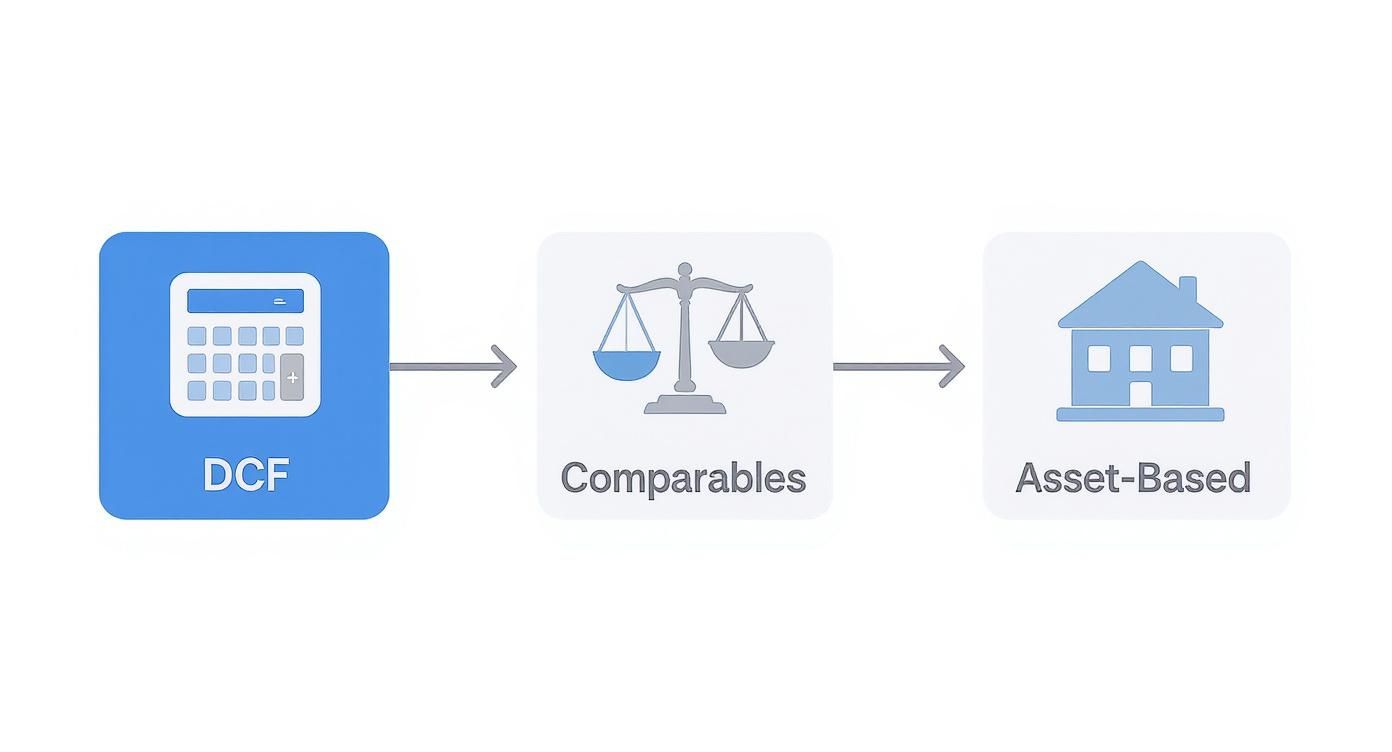

The infographic below shows how DCF fits alongside other common valuation methods. Each one gives you a different lens to look through.

As you can see, DCF is all about future cash (the calculator). Comparables, on the other hand, measure the business against its peers (the scales), while the asset-based approach is a straightforward tally of what it owns (the building).

Forecasting Future Cash Flows

Let’s be honest, this is the hardest part of any DCF analysis. You need to project the company's Free Cash Flow (FCF), which is the actual cash left over after the business pays for its operations and invests in its future. It's the pot of gold that could theoretically be handed out to investors.

Typically, you'll need to forecast FCF for the next five to ten years. This isn't just guesswork; it's about building a solid, data-backed story.

Start with History: Your first move should be to pull the last three to five years of financial statements. Pour over the income statement, balance sheet, and cash flow statement to spot trends in revenue, margins, and capital spending.

Build Realistic Assumptions: Where is the company headed? Project future revenue based on real-world factors like market growth, the competitive landscape, and the company's own plans. Don't just drag the past growth rate into the future—question whether it's truly sustainable.

Project Expenses and Investments: What will it cost to achieve that growth? You'll need to forecast everything from operating costs and working capital to the big-ticket capital expenditures needed for expansion.

To get this right, you really need to be comfortable with building robust financial models that can handle these moving parts without falling apart.

Determining the Discount Rate

Okay, so you have your cash flow projections. Now what? You have to bring those future numbers back to their value in today's terms. After all, a dirham in your pocket today is worth more than the promise of a dirham five years from now, thanks to risk and opportunity cost. That's where the discount rate comes in.

The go-to tool for this is the Weighted Average Cost of Capital (WACC). Think of WACC as the blended average rate of return the company must pay its lenders and shareholders.

A higher WACC signals more risk, which means future cash flows get discounted more heavily, leading to a lower valuation. A lower WACC implies less risk and a higher valuation. It's that simple.

Figuring out the WACC involves digging into the cost of equity, the cost of debt, and how the company is financed. Getting this number right is critical—even a small tweak can have a massive ripple effect on your final valuation number.

Calculating the Terminal Value

Most businesses are expected to keep running long after your five or ten-year forecast ends. The Terminal Value (TV) is your best estimate of the company's value for all the years beyond that forecast period. Don't underestimate its importance; it can easily account for over 70% of the total company value in a DCF model.

There are two main ways to tackle this:

Perpetuity Growth Model: Here, you assume the company's cash flows will grow at a slow, steady rate forever. This rate needs to be conservative—think in line with long-term economic growth, maybe 2-3%.

Exit Multiple Method: This approach pretends the company is sold at the end of your forecast. You calculate the terminal value by applying a market multiple (like EV/EBITDA) to your final year's projected numbers.

Which one should you use? It really depends on the industry and the specific company you're looking at.

A Practical DCF Example in Dubai

Let's put this into practice. Imagine we're valuing "DXB Logistics," a fictional tech-logistics startup in Dubai. Here’s how we'd approach it:

Project FCF: First, we'd map out its free cash flow for the next five years. We'd start with aggressive revenue growth, say 25% a year, but have it taper off as the business matures. We would also factor in heavy spending on new warehouses and a fleet of delivery vehicles.

Calculate WACC: For DXB Logistics, we might land on a WACC of 12%. This is fairly high, but it reflects the risk profile of a startup fighting for market share. It's certainly riskier than a well-established blue-chip firm.

Determine Terminal Value: Using the perpetuity growth model, we’d assume a stable, long-term growth rate of 3%, which is a reasonable proxy for the mature UAE economy.

Discount and Sum: Finally, we take each of those five years of FCF, plus the terminal value, and discount them all back to today's value using that 12% WACC.

Adding up these present values gives us the total enterprise value for DXB Logistics. From there, we just subtract its net debt to find the equity value.

Ultimately, the final number is only as good as the assumptions that went into it. That's why a rigorous valuation process often relies on thorough financial due diligence in Dubai to stress-test every input and ensure the result is both accurate and defensible.

Valuing a Business with Market Comparables

While a Discounted Cash Flow model has you looking inward at a company's own potential, the market comparables method forces you to look outward. This approach, often called Comparable Company Analysis (CCA), is built on a pretty straightforward idea: a company is worth what the market is willing to pay for similar businesses. It’s a powerful reality check that grounds your valuation in current market sentiment and what people are actually paying.

The whole process lives and dies by the quality of your "peer group"—the handful of publicly traded companies you choose to compare your business against. Honestly, this part is more art than science. You have to go beyond surface-level similarities to find businesses that are truly on the same wavelength in terms of operations, growth prospects, and risk.

Identifying Your True Peer Group

Choosing the right companies for comparison is, without a doubt, the most crucial part of the exercise. A poorly chosen peer group will give you a skewed valuation that’s unreliable at best and dangerously misleading at worst. You need to be methodical here.

I always screen potential comps based on a few core characteristics:

Industry and Sector: This is non-negotiable. The companies must operate in the same or a very similar industry. You wouldn't compare a software company to a heavy machinery manufacturer, even if their revenues match.

Business Model: How do they actually make money? A business with recurring subscription revenue has a totally different risk and growth profile than one that relies on one-off project sales.

Size: Try to compare apples to apples in terms of scale—look at revenue, total assets, or even employee count. A small, local retailer just isn't a good peer for a multinational hypermarket chain.

Geography: Market dynamics can be wildly different from one region to another. A company operating in the GCC faces unique opportunities and challenges that a similar business in North America simply doesn't.

Once you’ve put together a solid list of potential peers, it’s time to roll up your sleeves and get into their financials to calculate the valuation multiples.

Understanding Key Valuation Multiples

Valuation multiples are just financial ratios that connect a company's value to a specific financial metric. Think of them as a price tag based on performance, giving you different angles on what a company is worth.

EV/EBITDA (Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization) is a favorite among analysts for a reason. It strips out the noise from financing and accounting decisions, giving you a clean look at a company’s raw operating performance. This makes it fantastic for comparing companies that have different debt levels or tax situations.

The P/E (Price-to-Earnings) Ratio is probably the multiple everyone’s heard of. It compares a company's stock price to its earnings per share, telling you how much investors are willing to pay for each dollar of profit. But be careful—it can be misleading for companies with negative earnings or big non-cash expenses.

Finally, the P/S (Price-to-Sales) Ratio compares the company’s market cap to its total revenue. This is especially handy for valuing high-growth companies that aren't profitable yet, or for businesses in cyclical industries where earnings can swing wildly.

The goal isn't just to calculate these numbers; it's to understand the story they tell. A high EV/EBITDA multiple might point to strong growth expectations. A low P/E ratio could be a sign that a company is undervalued—or that it's facing some serious headwinds.

Applying Market Comparables in the GCC

When you bring this method to the GCC, you have to add a layer of local expertise. Global benchmarks are a good starting point, but you can’t ignore regional dynamics. The UAE, for instance, has become a major M&A hub, and that's changing how local companies are valued.

In a recent year, the UAE saw M&A deals worth about $25.4 billion in just the first half, which was around 43% of the entire MENA region's total. This flurry of activity, spurred on by reforms like allowing 100% foreign ownership, means UAE companies are increasingly being measured against international standards and often attract premium valuations.

The core principles of CCA don’t change, but how you apply them has to be specific. For a practical guide on performing these kinds of comparisons, which can even be applied to real estate, you can learn more about how to do a comparative market analysis.

To see how this plays out in the real world, just look at the different multiples across key sectors in our region.

Common Valuation Multiples by Sector in the MENA Region

The table below gives you a general idea of what to expect for valuation multiples in some of the MENA region's biggest industries. As you'll see, what's considered "normal" can vary dramatically from one sector to another.

Sector | Average EV/EBITDA Multiple | Average P/E Ratio | Key Considerations |

|---|---|---|---|

Technology | 15x - 25x | 25x - 40x | Valuations are often driven by high growth expectations and potential for market disruption. |

Energy | 5x - 8x | 10x - 15x | Highly sensitive to global commodity prices and government policies. |

Real Estate | 10x - 14x | 15x - 20x | Influenced by interest rates, population growth, and local economic sentiment. |

This table makes it clear: a "good" multiple is entirely dependent on the sector.

By carefully selecting your peer group, choosing the right valuation multiples, and layering on an understanding of local market conditions, you can build a valuation that is not only defensible but also truly reflects the company's standing in the market.

Getting to Grips with the Asset-Based Valuation Approach

While methods that look to the future, like DCF or market comps, often get all the attention, sometimes the most grounded way to figure out a company's worth is to simply look at what it owns. This is exactly what the Asset-Based Valuation (ABV) approach does. It's a method that cuts through the noise by adding up all of a company's assets and then subtracting its liabilities.

This approach is particularly useful for businesses whose value is intrinsically tied to their balance sheet. Think about manufacturing companies, real estate firms, or any capital-intensive industry. For them, tangible assets like property, machinery, and inventory are the heart of the operation. ABV also becomes the go-to method in less fortunate situations, like a liquidation, where future earnings are off the table and the only thing that matters is what the company's assets can fetch on the open market.

The Book Value Method: A Starting Point

The most straightforward version of asset-based valuation is the Book Value method. The math here is as simple as it gets: you take the total assets as they appear on the balance sheet and subtract the total liabilities. The number you're left with is the company's net book value, also known as its equity.

Easy, right? The problem is that while it's simple to calculate, it has a major blind spot. It relies on historical costs, which often don't line up with today's reality. A piece of machinery bought a decade ago might be nearly fully depreciated on the books, but if it's well-maintained and still in demand, it could be far more valuable. On the flip side, old inventory might be listed at its original cost but could now be practically worthless.

The Adjusted Net Asset Method: Getting Closer to Reality

This is where the more nuanced and widely accepted Adjusted Net Asset Value (ANAV) method comes in. Instead of just accepting the balance sheet figures, this approach requires you to roll up your sleeves and adjust each asset and liability to reflect its true, current fair market value.

It's definitely more work, but the result is a far more accurate snapshot of the company's actual worth. This process means taking a hard look at everything the company owns and owes.

Tangible Assets: Things like land and buildings are revalued based on current property appraisals. Equipment and machinery are assessed based on what they would sell for today, not their depreciated book value.

Intangible Assets: This is where things can get a bit tricky. You need to identify and assign value to assets that don't even appear on the balance sheet, like a strong brand reputation, patents, or valuable customer lists.

Liabilities: It’s not just about assets. All debts and obligations are also re-evaluated to reflect their current market value, which can include any off-balance-sheet commitments.

At its core, the ANAV method is about answering one fundamental question: "If we sold off every single asset at today's prices and settled every single debt, what would be left in the pot for the shareholders?"

Knowing the Limitations is Key

The asset-based approach isn't the right tool for every job. Its most significant weakness is that it often fails to capture the value of a business as a living, breathing, profitable entity—especially for companies in the service or tech industries.

For a software company, its most valuable assets—its proprietary code, the collective brainpower of its team, and its recurring revenue model—don't have a neat little box on the balance sheet. In cases like these, an asset-based valuation could drastically undervalue the company's true potential. That’s why we almost always use it alongside other methods, like DCF, to build a complete picture. The asset-based value often acts as a valuation "floor" or a baseline for a healthy, operating business.

For a more granular look at this process, our guide on valuing business plant and machinery offers a deep dive into this crucial component.

Real-World Example: A JAFZA Manufacturing Firm

Let's imagine a manufacturing company based in the Jebel Ali Free Zone (JAFZA). The company owns its factory building, a fleet of delivery trucks, and some highly specialized production machinery.

If we just used the Book Value method, the numbers might show a net worth of AED 15 million, based on what was paid for everything years ago.

But an ANAV analysis tells a much more compelling story. A professional appraisal reveals the factory's land and building are now worth AED 10 million more than their recorded book value. The specialized machinery, though not new, is in high demand and is actually valued at 25% above its depreciated cost.

After carefully adjusting all the assets and liabilities to reflect their current market prices, the Adjusted Net Asset Value lands at AED 28 million. This figure is a much more realistic and defensible number to take into a negotiation for a potential sale or a discussion with a lender.

Adapting Your Valuation for the GCC Market

If you apply standard valuation models to the Gulf Cooperation Council (GCC) market without local context, you're setting yourself up for failure. It’s a common mistake. This region moves to a unique economic rhythm, so a textbook approach to how to value a company can give you a number that’s miles off the mark. You absolutely have to adjust your analysis for factors that just don't carry the same weight elsewhere.

One of the biggest regional dynamics is the sheer influence of government-related entities (GREs) and sovereign wealth funds (SWFs). These are massive players in nearly every sector, from real estate and infrastructure to cutting-edge tech. Their investment decisions are often guided by long-term strategic goals—think economic diversification away from oil or ensuring national food security—rather than just chasing the highest immediate financial return.

What does this mean for you? It means they might pay a premium for an asset that a typical private investor would consider overvalued. This involvement can, and often does, inflate market multiples. It creates benchmarks that don't always reflect pure market fundamentals. When you’re running a comparable analysis, you have to dig deeper and ask: is this peer group's valuation skewed by a "sovereign premium"?

Navigating Local Risk and Regulatory Nuances

Beyond the influence of state-backed capital, a realistic valuation must bake in specific regional risks and opportunities. Geopolitical stability, the ever-present swings in oil prices, and sudden regulatory changes can directly hammer future cash flows and the discount rate you use.

For example, recent legal reforms allowing 100% foreign ownership in many sectors have been a game-changer. This fundamentally alters the risk profile for international investors, which can lead to a lower required rate of return and, consequently, higher valuations. On the other hand, the unique structure of the region's large, family-owned conglomerates demands a close look at governance and succession planning, which are often make-or-break valuation drivers.

When I'm working on a GCC-specific valuation, I always focus on these critical adjustments:

Country Risk Premium: Tweak your discount rate. You have to reflect the specific political and economic stability of the country where the business is headquartered.

Regulatory Landscape: You need to model the impact of localization initiatives (like Saudisation in KSA), the financial benefits of operating in a free zone, and sector-specific rules on long-term profitability.

Family Business Dynamics: For private companies, it's crucial to assess key-person risk. You also need to consider how an upcoming intergenerational wealth transfer might shift the company's entire strategic direction.

Valuing a company in the GCC isn't just about translating financial statements; it's about translating culture, policy, and strategic ambition into financial terms. Overlooking these elements means you're only seeing half the picture.

The Impact of Cross-Border M&A Activity

The valuation landscape here is also being dramatically reshaped by a surge in cross-border mergers and acquisitions. In a recent year, cross-border M&A in the MENA region soared to a five-year high, hitting 233 deals worth $45.9 billion. That figure accounted for a staggering 78% of the total deal value.

This flood of international capital means valuations now have to consider global supply chain integration and currency risk. This is especially true in hot sectors like technology and chemicals, which together contributed 67% of that deal value. Sovereign funds like ADIA and PIF were involved in transactions totaling $21 billion, which again shows how strategic government-led valuations can outpace private market analysis. You can get more details from these MENA M&A trends on consultancy-me.com.

All this intense M&A activity sets new, and often much higher, valuation benchmarks. A local tech startup, for instance, is no longer just being compared to its regional peers. Now, it’s being benchmarked against similar companies in Europe or Asia that have recently been acquired. It globalizes the entire process, forcing analysts like us to adopt a much wider perspective.

Ultimately, the key to an accurate and defensible assessment of a company's true worth lies in translating global valuation theory into on-the-ground GCC reality.

Common Questions We Hear About Company Valuation

Even with a solid understanding of the theory, the practical side of valuation always brings up questions. Getting these right is what separates a good valuation from a great one. Let's walk through some of the most common hurdles that analysts, founders, and investors face when trying to pin down a company's worth.

Which Valuation Method Is the Most Accurate?

This is easily the most common question, and the honest answer is: there isn't one. The biggest mistake you can make is relying on a single method, which can give you a completely skewed picture. The most credible valuations are built by using a few different approaches and seeing where they point.

We often present this as a "football field" analysis, which is just a simple bar chart showing the valuation ranges from each method. It helps visualize where the different techniques overlap.

A DCF tells you what the company is worth based on the cash it’s expected to generate in the future (its intrinsic value).

Market Comps show you how similarly-sized public companies are being valued by the market right now.

Precedent Transactions reveal what buyers have actually been willing to pay for comparable businesses in real-world deals.

A truly defensible valuation isn't a single magic number. It's a well-reasoned range where these different methodologies start to tell a consistent story. This triangulation gives you a much more solid foundation for making any major financial decision.

How Do You Value a Startup with No Revenue?

Valuing a company before it’s making money is a completely different ballgame. Your traditional models, which lean heavily on past performance or current profits, are useless here. The focus has to shift almost entirely from what the company is to what it could become.

Instead of crunching historical numbers, investors and analysts have to look at a different set of signals. The valuation becomes a narrative about future potential, backed up by early signs of promise.

What are they looking for?

The Founding Team's Strength: Is this a team that has the experience and grit to make it happen? This is non-negotiable.

Total Addressable Market (TAM): Just how big is the problem they're solving?

Intellectual Property: Is there a patent or some proprietary technology that gives them a genuine edge?

Early Traction: This is key. Things like user sign-ups, successful pilot programs, or key strategic partnerships act as a stand-in for revenue, showing that they're on the right track.

In practice, the final number is often benchmarked against what other pre-revenue startups in the same sector and region have raised in their funding rounds. It's about finding the current "market rate" for a promising venture at that stage.

What Common Mistakes Should I Avoid?

Most valuation errors boil down to one thing: bad assumptions.

It's easy to get carried away. An overly optimistic growth forecast that isn't tied to a realistic market opportunity can make a DCF model spit out an absurdly high number. On the flip side, using a discount rate that doesn't accurately reflect the company's risk profile will just as easily distort the outcome.

Another classic blunder is picking the wrong companies for your comparable analysis. If you're comparing your tech startup to established industrial giants, the multiples you get will be completely meaningless. You have to compare apples to apples.

Finally, a critical oversight, especially in the UAE and the wider GCC, is failing to account for the local economic and regulatory environment. A valuation that ignores these on-the-ground realities is one that’s fundamentally disconnected from the real world.

At Credence & Co., we provide unbiased, technically robust valuation opinions for financial reporting, transactions, and strategic planning. Our accredited experts combine international standards with deep regional knowledge to deliver precise analyses. De-risk your decisions by partnering with us. Learn more by visiting our website.

Comments